📰IT'S FED WEEK AND BIG JOB NEWS UPDATE 📰

THIS WEEK’S MARKET MOVING NEWS FOR THE WEEK OF JULY 29TH

July 29, 2024

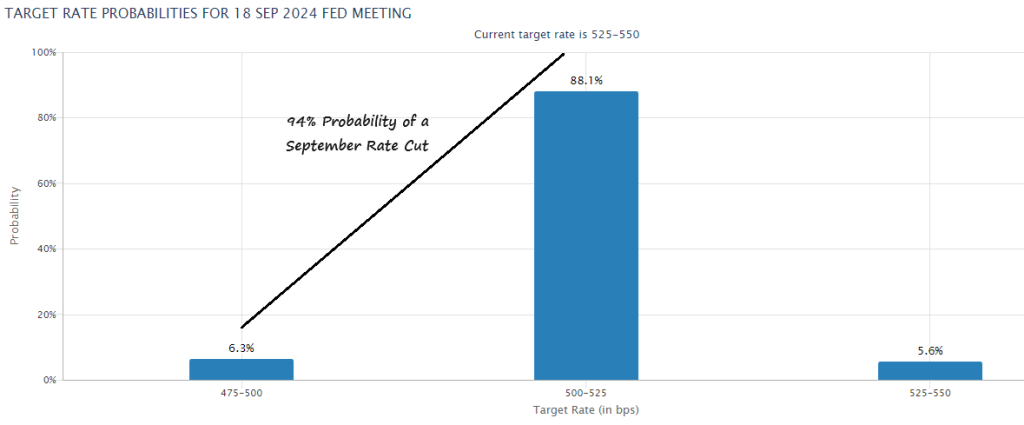

This week is set to be crucial for the financial markets, with several significant events on the agenda. The Federal Reserve's two-day meeting begins tomorrow, culminating in a statement and press conference by Jerome Powell on Wednesday at 2:00 PM ET. While it's broadly expected that the Fed will not cut rates at this meeting, they are likely to set the stage for a potential rate cut on September 18.

Nick Timiraos of the Wall Street Journal, often dubbed the "Fed mole," published an article last night titled “A Fed Rate Cut Is Finally Within View.” In it, Timiraos outlines why the Fed might be preparing for a September cut:

Inflation Progress: Inflation has shown improvement, boosting the Fed's confidence in achieving its 2% target.

Cooling Labor Market: The unemployment rate has risen over the past three months to 4.1%, indicating a cooling labor market.

Risk of Delay: Jerome Powell is concerned about the risks of delaying a rate cut, which could lead to economic weakness or a recession.

The general expectation is that the Fed will keep rates unchanged but adopt a dovish tone, acknowledging progress in inflation, a cooling labor market, and signs of a slowing economy.

In job market news, the ADP and BLS reports are expected to show 149,000 and 175,000 jobs created in July, respectively, with the unemployment rate projected to remain at 4.1%. However, the jobs report is notoriously unpredictable, often overstating job growth only to revise figures down later. A higher-than-expected job creation number could dampen bond market optimism, whereas figures in line with or below expectations could spark a bond market rally.

An unexpected rise in the unemployment rate to 4.2% could surprise many Fed members and potentially lead to a more aggressive rate cut in September.

Key Events to Watch This Week:

Tuesday: CB Consumer Confidence data, JOLTs Job Openings data

Wednesday: Fed Rate Decision and Statement

Thursday: ISM Manufacturing PMI data

Friday: June Jobs Report

Throughout the Week: Earnings reports from about 20% of S&P 500 companies

Given this packed schedule, significant market volatility is anticipated. The job reports, in particular, are a wild card. We hope for lower-than-expected new job creation and a higher-than-expected unemployment rate to support a rate cut in September, especially following a flat inflation report last week.

In summary, this week will likely be stressful in the headlines, but the good news is that the likelihood of lower rates has never been stronger since late 2022. We're getting there, even if the final stretch is slow.

ARE HOME PRICES CRASHING?

There are many confusing headlines about home prices, with terms like "crash" or "correction" being thrown around. These words can negatively impact your perception of the market. However, home prices aren’t going to come tumbling down. National data shows that prices are normalizing and will continue to climb, just at a slower pace.

During the pandemic, home prices soared due to high demand, low inventory, and low mortgage rates. This rapid appreciation was unsustainable, and now, data confirms that prices are still rising, but more moderately. This healthier pace is beneficial, signaling that home price growth is normalizing.

Danielle Hale, Chief Economist at Realtor.com, explains:

"In stock market terms, a correction generally refers to a 10 to 20% drop in prices. We don't have the same established definitions in the housing market."

In today’s housing market, a "correction" doesn’t mean dramatic price falls. It means that prices, which have been increasing rapidly, are now growing at a slower pace. While prices vary by local market, a significant national drop isn't happening.

From 2020 to 2022, home prices skyrocketed due to high demand, low interest rates, and a shortage of homes for sale. Such aggressive growth couldn’t last forever. Today, the price growth is slowing down, indicating market normalization. The most recent data from Case-Shiller shows prices are rising at a national level, but not as quickly as before. This year, price growth has been healthier compared to the pandemic years.

Looking ahead, Marco Santarelli, Founder of Norada Real Estate Investments, says:

“Expert forecasts lean towards a moderation in home price growth over the next five years. This translates to a slower and more sustainable pace of appreciation compared to the breakneck speed witnessed in recent years, rather than a freefall in prices.”

It always boils down to supply and demand. Increasing inventory and limited buyer demand, due to relatively high mortgage rates, will continue to ease upward pressure on prices. As mortgage rates improve, it’s uncertain if the supply can outpace demand to drive prices down significantly. A surplus of supply is needed to shift into a buyer’s market.

If you’re thinking about buying a home, slowing price growth is welcome news. For many buyers, this is the exact headline we’ve been waiting for. Skyrocketing home prices during the pandemic left many would-be homebuyers feeling priced out. Now, while home values will likely continue to rise once you own a home, slowing price gains make homeownership more manageable.

Odeta Kushi, Deputy Chief Economist at First American, says:

“While housing affordability is low for potential first-time home buyers, slowing price appreciation and lower mortgage rates could help — so the dream of homeownership isn't boarded up just yet.”

At the national level, home prices are not going down, and most experts forecast moderate growth moving forward. Prices do vary by local market, which is why consulting a trusted real estate agent is crucial. If you have questions about what’s happening with prices in your area, reach out for personalized advice. I have tools available to help. Always remember, the best time to buy a home is when you’re buying within your means.

WEALTH AND HOMEOWNERSHIP

A significant wealth gap exists between renters and homeowners due to the equity homeowners build as their property values appreciate and they make mortgage payments. Homeownership acts as a form of forced savings, providing a financial return when the home is sold. In contrast, renters do not gain any financial benefits from their monthly rent payments. Ksenia Potapov, Economist at First American, highlights that renters miss out on wealth generated by house price appreciation and equity gains from mortgage payments.

Home equity is a crucial component of most homeowners' net worth, significantly boosting wealth across all income levels. Data from First American and the Federal Reserve show that home equity makes up a large part of a homeowner's net worth. Nicole Bachaud, Senior Economist at Zillow, emphasizes that homeownership is a key financial asset that promotes stability and wealth preservation across generations.

If you're considering building your net worth, the current real estate market offers opportunities such as lower mortgage rates and increased inventory. A local real estate agent can help you navigate these opportunities and find your ideal home. Owning a home can enhance your overall wealth in the long run, regardless of your income level.

When you consult with me, I can show you exactly how to prepare for sustainable financing and successful homeownership.

ARE CRE MORTGAGE DELINQUENCIES DECLINING?

Delinquency rates for commercial mortgages showed a slight improvement in the second quarter despite a challenging economic environment.

Here's what happened: The Mortgage Bankers Association (MBA) reported that the overall delinquency rate for commercial mortgages 60-90 days overdue dropped by one basis point to 0.2% in Q2. Additionally, 97% of outstanding loan balances were current or less than 30 days late, a slight increase from 96.8% in Q1. The percentage of loans 90+ days delinquent or in REO remained steady at 2.5%.

Between the lines: Jamie Woodwell, MBA's head of commercial real estate research, noted that delinquency rates declined for most property types, except office properties, which saw an increase. However, the pace of delinquencies for office property loans has slowed recently.

Breakdown of Delinquency Rates by Property Type:

Office Properties: Delinquencies increased to 7.1%, up from 6.8% in Q1.

Lodging Loans: Decreased to 5.8% from 6.3%.

Retail Balances: Dropped to 4.5% from 4.7%.

Multifamily Balances: Fell to 1.1% from 1.2%.

Industrial Property Loans: Reduced to 0.8% from 1.2%.

The takeaway: Looking ahead, Woodwell added, "Commercial properties are navigating a unique set of challenges shaped by fluctuating interest rates and property values. Each loan and property will need to adapt to evolving conditions based on specific factors like property type, market trends, and loan terms. Further adjustments are expected as more loans reach maturity throughout the year.

LET’S CONNECT

Going Beyond The Headlines...

The primary objective of my newsletters is not to induce fear but rather to ensure you stay well-informed about the current state of the real estate market. My goal is to go beyond the headlines and provide you with a deeper understanding of the truth behind the market trends. By offering comprehensive insights, I aim to empower you to make informed decisions regarding your real estate investments. Transparency and accuracy are at the forefront of my approach, ensuring that you have access to reliable information that goes beyond mere sensationalism.